Risk Center Ambassador

Prof. em. Paul Embrechts serves as the Ambassador for Risk at the Risk Center and RiskLab. He is a founding member of the Risk Center and was a member of the Steering Committee from 2011 to 2018.

Paul Embrechts studies concepts, techniques and tools of Quantitative Risk Management, applied mainly (but not solely) to the financial industry (insurance and banking). The modeling of extreme events, both in size and interdependence, is a key aspect of the mathematical research carried out at RiskLab.

An important component of his current work is the public communication and understanding of risk.

Read more about Paul here

November 2022

OnlineTalk on November 16: "Theory and Applications of Extreme Value Theory", in the new series of Stochastics Seminars at Amirkabir University of Technology, Tehran, Iran.

October 2022

Talk on October 11 on the occasion of the conference in memory of Tomas Bjoerk at the Swedish House of Finance, Stockholm.

Talk on October 14: "Experiences from establishing RiskLab and the Risk Center at ETH Zurich", Inauguration of The Finance Research Day, TU Delft, The Netherlands

September 2022

Tutorial on September 4: "Risk Revealed: Cautionary Tales, Understanding and Communication", DPG-Tagung of the Condensed Matter Section (SKM), September 4 - 10, 2022, University of Regensburg, Germany

July 2022

Keynote Speech on July 5: "From Robust Risk Management to Evidence Based Communication", International Conference on Robust Statistics (ICORS 2022), July 5-8, 2022, University of Waterloo, Canada.

May 2022

Talk on May 24: "The Understanding and Communication of Extreme Risk", Keynote Speaker at the 75th Anniversary of the Portuguese Association of Actuaries, Lisbon, Portugal.

Talk on May 20: "Finding opportunities outside academia", Invited discussant at the Forum Lunch Panel of the Zurich Graduate School in Mathematics, Zurich.

Podcast Interview on May 19: "Risk Communication" with students following the ETH MTEC course "Introduction to Risk Modelling and Management".

Zoom-Talk on May 18: "Managing risk under What If constraints", Invited Speaker at the School Risk and Actuarial Studies of the Business School of the University of New South Wales, Sydney, Australia.

Workshop on May 12: "Statistics and its Role in Societal Challenges", Invited Round Table discussant organised on the occasion of the 30th Anniversary of the Institute of Statistics, Biostatistics and Actuarial Sciences at the University of Louvain-la-Neuve, Belgium.

Zoom-Talk on May 4: "Model and Decision Uncertainty for Catastrophic Events", at the London School of Economics in the Seminar on Uncertainty and Insurance Decisions.

April 2022

Talk on April 27: "Risk Revealed. Cautionary Tales, Understanding and Communication" at DNV Oslo and University of Oslo

Presentationon on April 27: "Perspectives of Risk Management" at the Swiss Embassy, Oslo

March 2022

Talk on March 30: "Risk optimization under what-If constraints", a zoom-talk at the Institute for Mathematical and Statistical Innovation (IMSI), Chicago, USA. Scientific Program: "Decision Making and Uncertainty".

February 2022

Talk on February 28: "From the Bell Curve to Power Laws: A brief encounter with Extreme Value Theory" a 90' zoom-talk for the D-MTEC course on "Risk Modeling and Management"

Talk on February 7: "Risk, Told: Cautionary Tales, Understanding and Communication" at SAV Bahnhofskolloquium, Zurich

October 2021

Zoom-Talk on 15 October: "The Public Understanding and Communication of Risk - Part II", at the Analysis Seminar of West Michigan University, West Michigan University, USA

Zoom-Talk on 8 October: "The Public Understanding and communication of Risk - Part I", at the Analysis Seminar of West Michigan University, West Michigan University, USA

Talk on October 1: "Risk, Told: Cautionary Tales, Understanding and C ommunication" at the conference Contributions in extreme value statistics - estimating the tail of the survival function and its relevance in finance, insurance and environmental statistics in honour of the retirement of Professor Jan Beirlant, KU Leuven, Department of Mathematics, Belgium

September 2021

Zoom-talk on September 28: "The Public Understanding and Communication of Risk" at the German Probability & Statistics Days Mannheim, September 27 - October 1, 2021

Zoom-Talk on 17 September: "From "If" to "What If": EVT as a Risk Management Tool" at The NUS Joint Seminar in QuantitativeFinance Series, National University of Singapore, Department of Mathematics and Risk Management Institute

August 2021| ITAM - Instituto Technologico Autonomo de Mexico

Zoom-Seminar on 20 August: The Fundamental Theorem(s) of Quantitative Risk Management, El Departmento de Actuaria y Seguros, Mexico

April 2021| Leuven, Belgium: and& Festival 2021, 21-25 April

Round table discussion on 21 April: Can Financial Greed be Beneficial for Everyone?

Participants: Véronique Goossens (Belfius), Wim Schoutens (Leuven), Nicholas N. Taleb (New York) and Paul Embrechts (Zurich).

March 2021| Uncertainty and Risk: A virtual workshop to commemorate a century of publication of Frank Knight's "Risk, Uncertainty, and Profit" and John Maynard Keynes' "A Treatise on Probability"

University of Oxford and Alan Turing Institute, March 17-19

Zoom-Talk on 19 March: Invited discussant, round table on "The Roles of Statistics and Data Sciences in Economics", University of Oxford and Alan Turing Institute

Zoom-Talk on 17 March: Invited talk "Dependence Uncertainty and Risk", University of Oxford and Alan Turing Institute

January - February 2021| Analysis Seminar of West Michigan University

Zoom-Talk 2 on 5 February: The Second Fundamental Theorem of Quantitative Risk Management: Wall Street Reality, West Michigan University, USA

Zoom-Talk 1 on 29 January: The First Fundamental Theorem of Quantitative Risk Management: Mathematical Utopia, West Michigan University, USA

December 2020 | Texas Tech University, USA

Zoom-Talk on 1 December: The Fundamental Theorem of Quantitative Risk Management, Texas Tech University, USA

November 2020

Zoom-Talk on 19 November: Public Lecture, The Statistical Analysis of Extreme Events, Educational University of Hong Kong and Hong Kong Statistical Society

Bluejeans-Talk on 13 November: Operational Risk and Model Uncertainty, Pictet, Geneva

Zoom-Talk on 10 November: The Public Understanding and Communication of Risk, ETH Risk Center Seminar Series, Zurich

August 2020 | Enterprise Risk Management Conference, Actuarial Society of South Africa, Johannesburg, South Africa

Zoom-Talk on 6 August: Keynote Lecture: Revisiting Operational Risk: from Basel to the Coronavirus

July 2020 | Séminaire Virtuel de Mathématiques Actuarielles et Financières, Quantact-CRM, Montréal

Zoom-Talk on 8 July: Hawkes Graphs: The Analysis of Large Multitype Event Streams

June 2020 | Technische Gesellschaft Zürich

Zoom-Talk on 22 June: Holländische Deiche und Finanzkrisen

May 2020 | Bachelier Finance Society One World Seminar

Zoom-Talk on 7 May: Operational Risk revisited: from Basel to the Coronavirus

March 2020 | Zurich Insurance Group and ETH Risk Center/D-MTEC

Talk on 18 March: Extreme Events as a Basis for Risk Quantification

February 2020 | The Swedish Society of Actuaries, Stockholm

Talk on 12 February: The Fundamental Theorem of Quantitative Risk Management

January 2020 | ETH Zurich

Talk on 27 January: Holländische Deiche und Finanzkrisen

ETH Zurich – Emeritenstamm – Winterthur Download slides (JPEG, 248 KB)

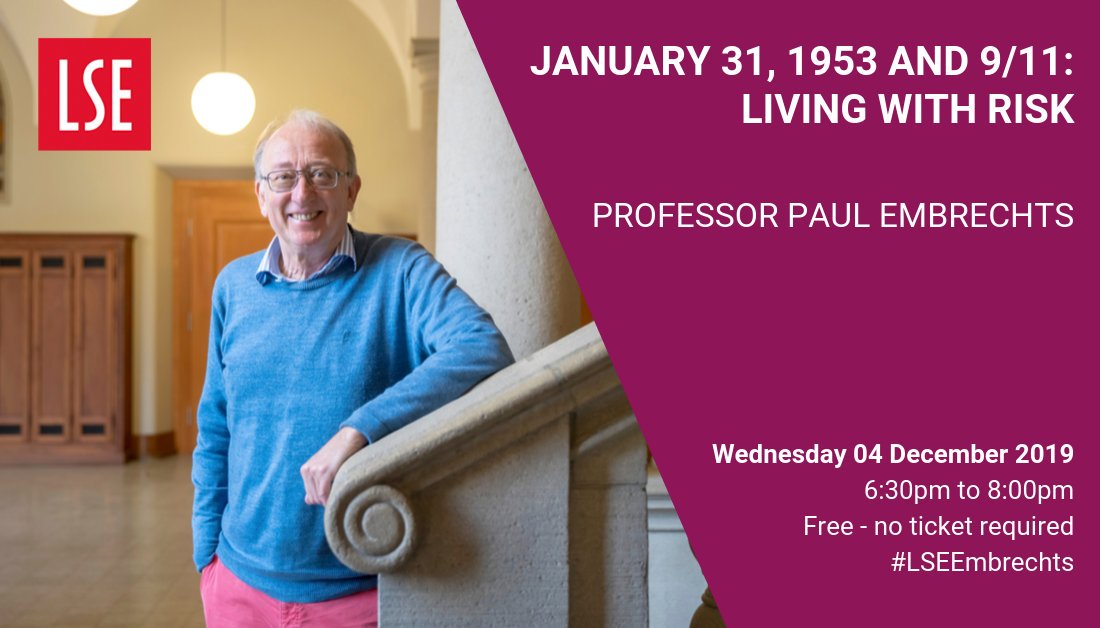

December 2019 | Visit at LSE, London

Public Lecture on 04 December

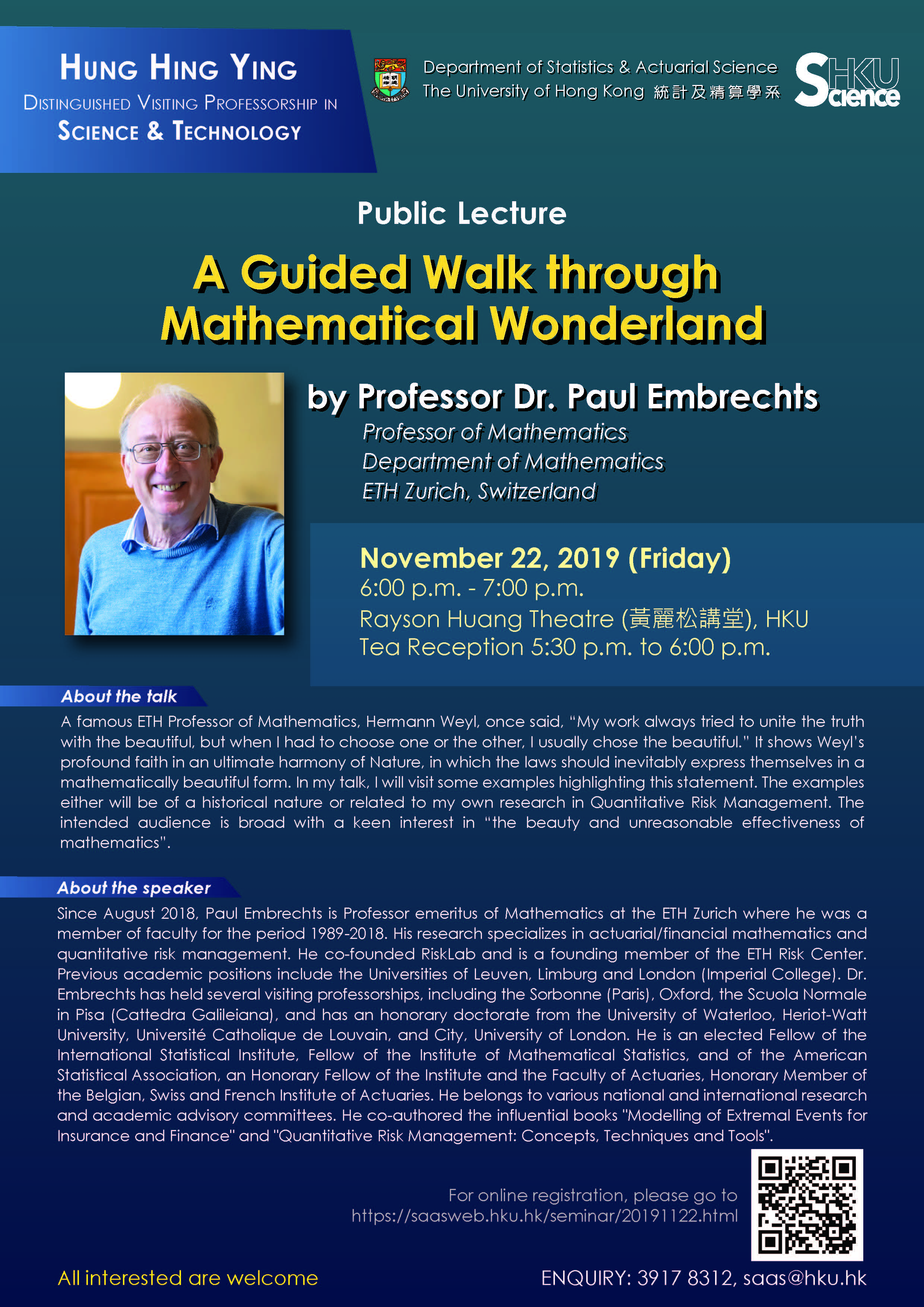

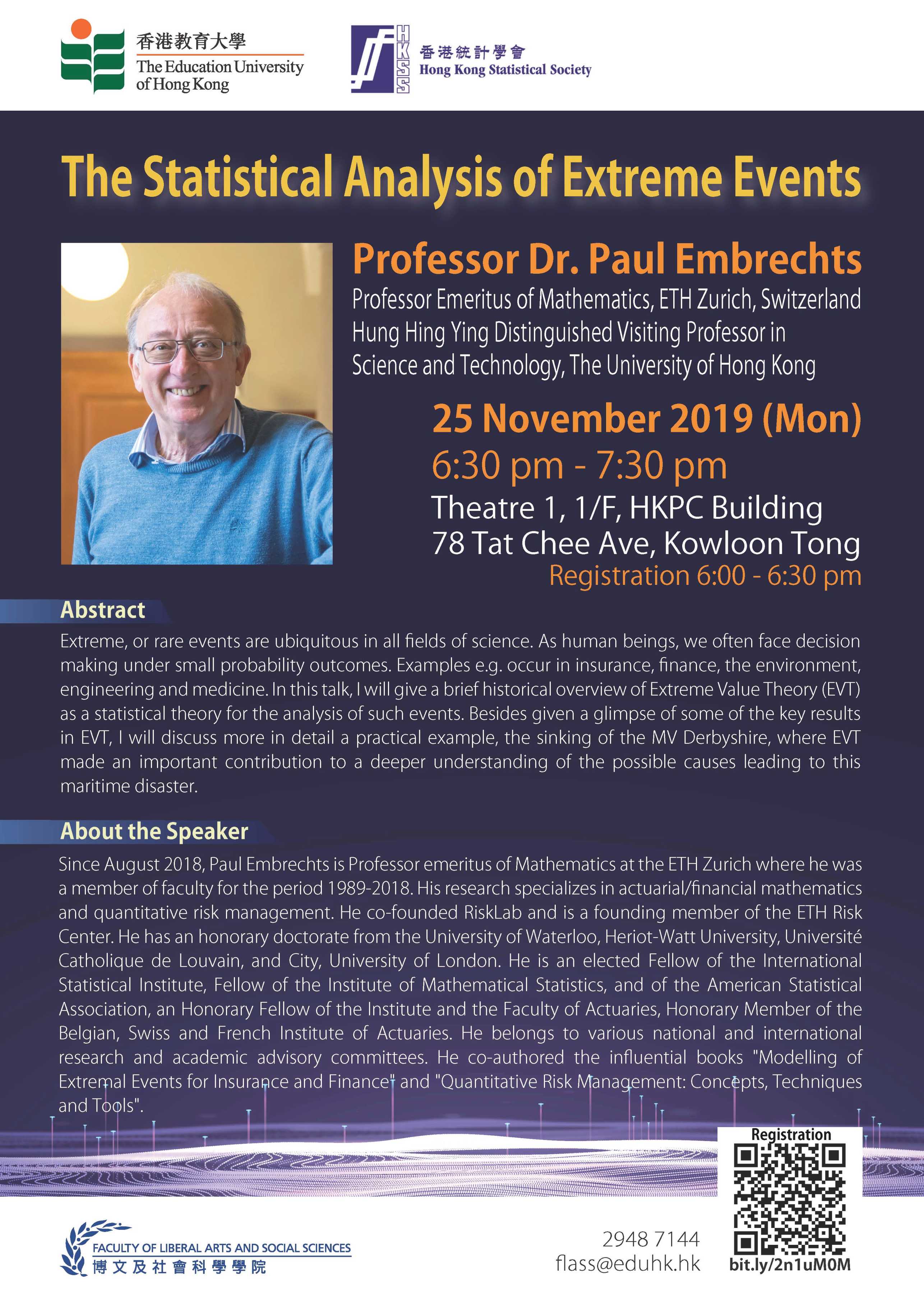

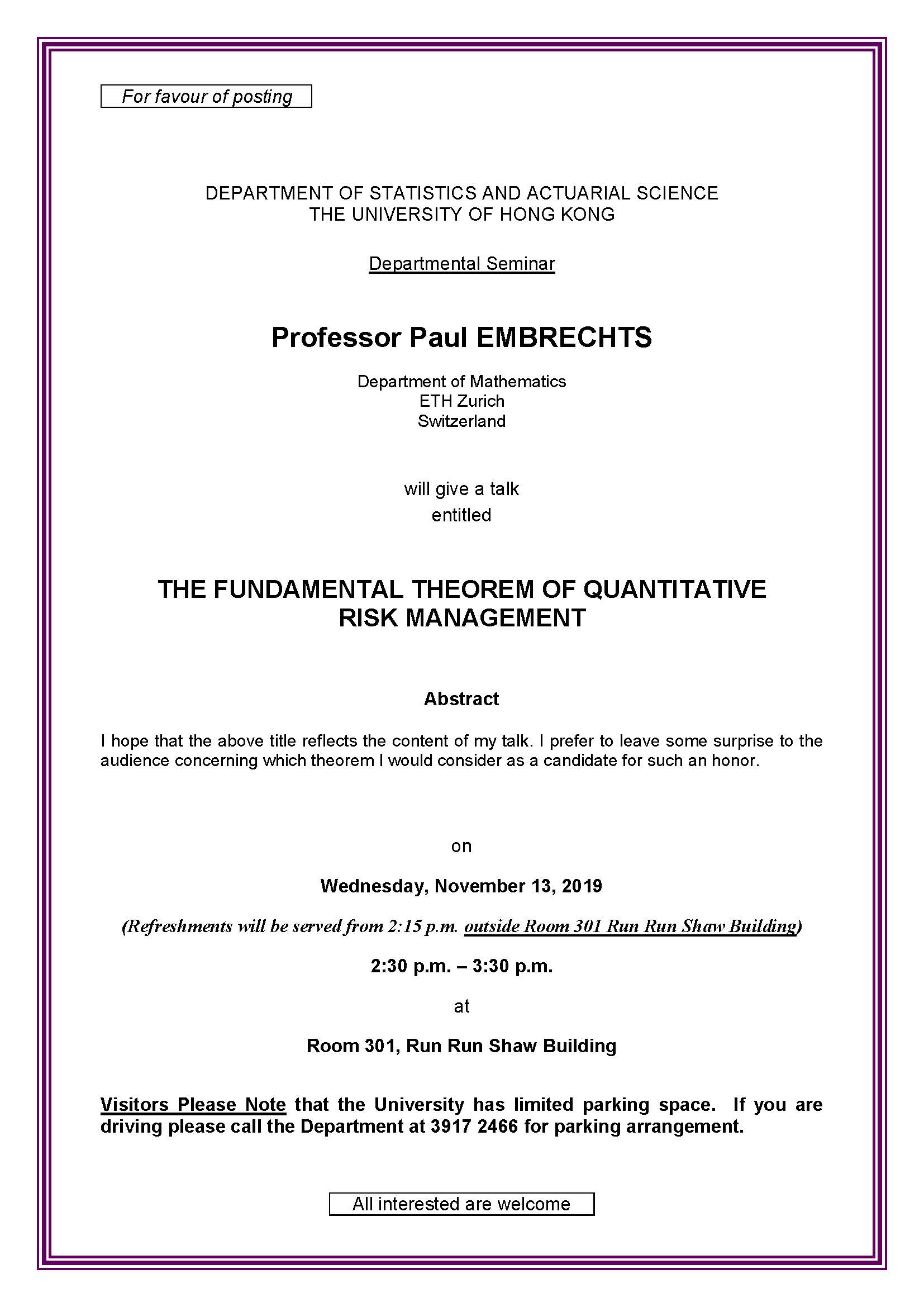

November 2019 | Visit at The University of Hong Kong, Department of Statistics and Actuarial Science

Talk on 13 November: The Fundamental Theorem of Quantiitative Risk Management (zoom-version: 17 June, 2020)

Talk on 22 November: A Guided Walk through Mathematical Wonderland (zoom-version: 24 June, 2020)

Talk on 26 November: The Statistical Analysis of Extreme Events

September 2019 | Vienna Congress on Mathematical Finance, WU Vienna, 9-11 September

Plenary Lecture on "Hawkes Graphs: A graphical tool for the analysis of multi-typr rvrnt streams", 9 September

August 2019 | Workshop on "Quantitative Finance: Asset Pricing and Risk Management", NUS Singapore (Risk Management Institute and Institute for Mathematical Sciences), 26-30 August

Tutorial on "The First and Second Fundamental Theorem of Quantitative Risk Management", 26 August

Invited Talk: "Risk-sharing, Robustness and Regulation", 29 August

July 2019 | 23rd International Congress on Insurance: Mathematics and Economics, TUM Munich, Germany

Opening Lecture "The Fundamental Theorem of Quantitative Risk Management", 10 July

June 2019 | 3rd European Congress of Actuaries, Lisbon

Opening Lecture: "Living on the Edge" 21 years on, 6-7 June

May 2019 | Conference in honor of Nicole El Karoui, 3x25 birthday, Sorbonne University, Jussieu Campus, Paris

Talk on "Operational Risk revisited", May 23

Round Table (moderator): "Women in Science: les femmes scientifiques sortent de l'ombre", 21 May

April 2019 | HEC - University of Lausanne

Talk on "Risk-sharing, Robustness and Regulation", 24 April, 2019, University of Lausanne.

April 2019 | University of Pécs, Hungary

Talk on "The actuarial profession in a changing risk landscape: some challenges", 15 April, University of Pécs, Hungary.

March 2019 | University of Cambridge

Talk on "Hawkes processes with applications to high-frequency finance", Cambridge-INET conference on Score-driven and nonlinear time series models.

March 2019 | Lecture on Extreme Events

Risk Center Lecture at ETH Zurich on "Introduction to Risk Modelling and Management".

Feb 2019 | Dutch National Bank

Talk on "How to, or not to handle Operational Risk", Dutch National Bank, Amsterdam.

Feb 2019 | Erasmus University Rotterdam

Talk on "Risk-Sharing, Robustness and Regulation", Tinbergen Institute of Erasmus University Rotterdam.

Paul Embrechts wins "Paper of the Year 2018" Award

The Award for "The 2018 Paper of the Year on Operational Risk" was given to Paul Embrechts for his paper "Modelling Operational Risk depending on covariates: an empirical investigation" co-authored with Kamil Mizgier and Xian Chen, published in the Journal of Operational Risk in March 2018. For details of the award, see Download here (PDF, 396 KB).